Ronda, Spain

Since publishing the first MIMOSA report – on Cambodia – I’ve heard one persistent critique. We say that the market is saturated, yet none of the current indicators appear to support it: repayments are great, there’s no field evidence of widespread overindebtedness, and the major MFIs are all undergoing a process of Smart Certification. How can we assert that Cambodia is at risk of overindebtedness, let alone a credit crisis, when no other indicators seem to support it?

These are important and reasonable questions. But here’s the rub – all the factors that point to a healthy market are either lagging indicators or are too vague or too poorly understood to be used as benchmarks.

First, if there’s one thing I’ve learned over the years of studying credit bubbles – starting with my work in the US mortgage sector during 2001-2008, through Andhra Pradesh, Morocco, and others – it’s that delinquency should never be used an indicator of a bubble. Rising delinquency is an important warning signal, certainly – but what it signals is that the bubble has begun to burst. From there on, it’s all about crisis management. What MIMOSA seeks to do is to avoid getting to that stage in the first place.

As with delinquency, so with client surveys seeking to assess overindebtedness. Here too we have a dilemma – there is no standard metric for measuring financial stress. First, we should recognize that any microfinance market, no matter how healthy, will show a significant number of clients experiencing financial stress. That’s simply a function of poverty. Markets with no microfinance or any formal lending will show this too. What we don’t know is to what extent loans are contributing additional stress that wouldn’t be present otherwise. Even measuring stress stemming directly from loan repayments isn’t sufficient. A client borrowing to pay for sudden health emergency may suffer repayment stress, but it is perfectly plausible that this level of stress is lower than what the client would’ve experienced had she not been able to borrow.

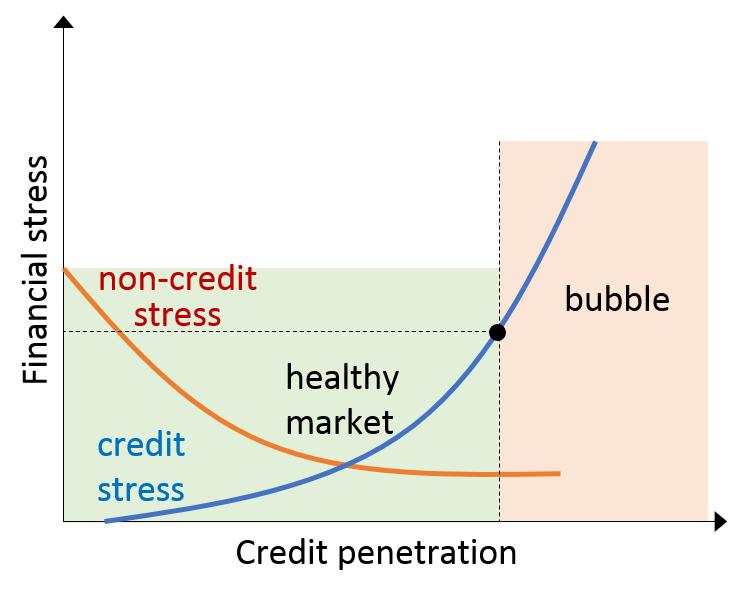

In theory, credit markets should follow a U-shaped pattern. More credit will inevitably create more credit-related stress, but presumably it will compensate by reducing non-credit stress even more (were this not the case, it would be an argument for eliminating all credit!). However, as penetration increases, at some point credit will start to create additional stress in excess of the non-credit stress it replaced. That would be the start of the bubble. But where that point lies is extremely difficult to assess. It’s influenced by a multitude of factors, including the local market context, type of credit provided, the level of credit concentration, and much else.

What’s particularly challenging is that in a healthy market we would expect to have some level of credit stress. So measuring that alone is not enough. Nor is there a sufficient number of comparable stress observations from multiple markets at multiple points in time from which to create benchmarks. Instead, we rely on a range of proxies to help guide us – the approach behind MIMOSA.

Criticisms arguing that MIMOSA may be overstating saturation and overindebtedness risk in markets like Cambodia are in essence saying that this market hasn’t yet arrived at that point of inflection where a healthy market has become a bubble. I agree that we haven’t precisely determined this point. But neither has anyone else.

Indeed, such a point will never be precisely defined. Credit markets are not like the physical world, where one can live perfectly safely on the edge of a precipice, enjoying the awe-inspiring views. The precipice we seek to define will forever be shrouded in mist. The best we can do is build tools like MIMOSA that act as an imperfect radar to describe that which cannot be seen. I welcome challenges of those areas where MIMOSA falls short. But for now, this is the best tool available, and what it shows in Cambodia is a market that has either already passed into the realm of bubble or is close to it. The critique that we’re overshooting is essentially an argument for relying on uncertainty to maintain the status quo, meaning continuing high competition and rapid growth.

The ultimate purpose of risk management is to deal with uncertainty. That includes taking reasonable precautions when sufficient warning signs are present. Given the risks in Cambodia, those reasonable precautions should include getting a better handle on competition, accompanied by a substantial slowdown in growth.

Yes, rolling out Smart Certification across the sector can help. Indeed, back in 2012, I proposed this very idea for Cambodia. But even if this process does succeed in certifying all major MFIs, that alone is no guarantee that a market crisis will be avoided. We have seen the rapid rise of newcomer MFIs like Ly Hour and some commercial banks entering the arena and changing the dynamics of competition. Despite its value, Certification is not nearly strong enough to contain the destabilizing force created by the continued and rapid expansion of credit.

There is only one prudent course – the market in Cambodia must be slowed, and soon. Back in 2009, when writing about the signs of building bubble in Andhra Pradesh, I warned:

The path being taken by Cambodia is by no means the same as in Andhra Pradesh. Many lessons have indeed been learned. But the risk of continuing rapid growth in a crowded and saturated market is one that should be heeded most of all.

Dear Danel, thatk you again for your excellent post … I don;t have much knowledge about Cambodia. But ‘commercialization’ of microfinance is indeed becoming the real challenge in many contexts, including in African markets. Especially where there is no good regulatory framework, or no prudent supervisions of grass-root level microfinance operations, this is likely to happen. Given the level of ‘financial literacy’ of the poor in many contexts, especially in rural areas, we cannot say that the poor can make ‘rational’ decision on financial needs. … But are microfinance institutitutions directly responsible to such financial literacy issues,or is this a ‘public good’ to be managed by governments, etc …Regards, Getaneh

Thanks Getaneh, appreciate the feedback. From my perspective this isn’t a strictly commercial vs. non-commercial issue. There are examples of highly competitive NGO MFIs destabilizing markets. Morocco 2005-08 is a perfect example of this (though I don’t view the situation as exactly a “bubble” in the vein of Bosnia, Nicaragua, or Andhra Pradesh). Though NGOs do seem as a rule less likely to get into an unsustainable competitive dynamic, and when they do, they are also more likely to be able to pull away as in Bangladesh circa 2008 (see CGAP paper “A Microcredit Crisis Averted: The Case of Bangladesh“).

But neither am I willing to relegate poor-oriented financial services solely to NGOs. In all cases, the sectors need good oversight and regulation. That alone should go a long way.

In general, given the low levels of financial literacy in poor communities, I believe it is the duty for MFIs to offer their customers customized financial literacy as a prerequisite for them to access financial products and services, especially credit products.