Some lessons are unexpected. Back in 2000, during the height of internet stock craze, I was an amateur manager of a small stock fund consisting of 8 smalltime shareholders who were all my relatives. Being a bit of a contrarian, the fund focused mainly on biotech stocks, which were enjoying quite a strong run, even if not quite as exuberant as dotcom stocks. The fund did well – a roughly 250% return over 3 years, but as always, the lesson was not from this relative success, but from a far larger failure – the missed opportunity to bank a 750% return.

Some lessons are unexpected. Back in 2000, during the height of internet stock craze, I was an amateur manager of a small stock fund consisting of 8 smalltime shareholders who were all my relatives. Being a bit of a contrarian, the fund focused mainly on biotech stocks, which were enjoying quite a strong run, even if not quite as exuberant as dotcom stocks. The fund did well – a roughly 250% return over 3 years, but as always, the lesson was not from this relative success, but from a far larger failure – the missed opportunity to bank a 750% return.

One stock stands out in my mind: Incyte Pharmaceuticals, which I had bought variously when it was trading in the $10-$20 range during 1998-99. By early 2000, it had crossed $100/share and was rapidly heading higher. At the time, I was well aware that there was no fundamental reason behind this runup – it was classic speculation. The question was when to sell? Internally, we had set a target of $150 (at a time when it was nearing $140 and rising rapidly). It was not to be. We sold some weeks later when it had slid down to the $60s…

Call me greedy and stupid. But I learned my lesson – I’m not made for stock trading! More importantly, it was my first introduction to the dangers of inexorable growth, which creates expectations that are difficult to reset and that far too often lead to disaster.

No, I’m not implying that microfinance in Cambodia or elsewhere is a dotcom-level bubble. But what’s at work is the basic mathematical principle – sustaining a high growth rate becomes increasingly difficult over time. A young industry may well grow 30%-40% annually for many years; for a mature one, this is nearly impossible. And all young industries mature eventually, so growth must necessarily slow.

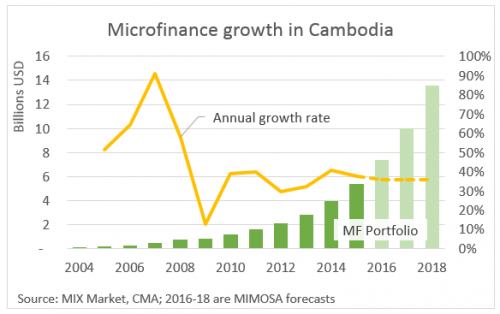

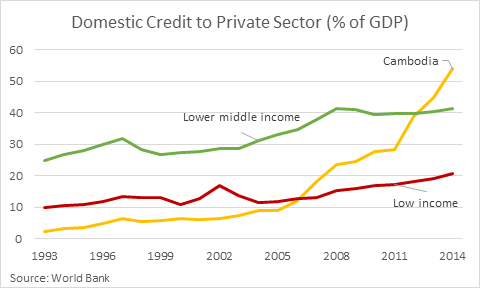

Watching Cambodia over the past several years has become increasingly uncomfortable for this very reason. Its MFIs have been averaging annual growth of 45% since 2004. And while they started small, that is no longer the case. Even so, as of Q1 2016, they posted 41% year-over-year growth – and show no sign of slowing. The $1.4 billion growth in loan portfolio in 2015 was larger than the entire market in 2011. The answer from MIMOSA is simple – not much longer. Now would be a good time to slow down. A lot. But let’s set aside MIMOSA and look at a different perspective that’s more commonly used by macroeconomists – domestic credit to the private sector as a share of the economy. On that score, Cambodia is yet again an outlier on several fronts. As of 2014, domestic credit to private sector in Cambodia stood at 54% of GDP. Given the growth since then, it’s probable that this figure is now over 60%. That puts Cambodia well above the average for its peer group of lower-middle income countries, which currently stand at 41% credit/GDP. And in that group, Cambodia is one of the very poorest countries, having just graduated from the low-income country group in 2014. Thus, whereas a peer comparison might place Cambodia somewhere between the low-income and lower middle-income levels, i.e. credit/GDP ratio of around 30%, it currently stands at twice that level. It’s not just the level of credit penetration that separates Cambodia from its peers. Its growth rate makes it an outlier as well. For the past decade, Cambodia has increased its credit/GDP ratio by 45 points, up from 9% in 2004. What’s the peer group for that type of growth? We took a look, and despite going back to 1980, the list is remarkably small:[2] Period Credit/GDP Ratio Situation/ Outcome Start End Among these, Brazil and Zimbabwe were both symptoms of hyperinflation and thus have no relevance for Cambodia. Another two (Armenia and Mongolia) are essentially ongoing, and thus can’t be used as historical evidence. Nepal’s and Serbia’s rapid run was not really growth, but simply a rebound back to an earlier level. Of the remaining nine, five (Bolivia, Bosnia, Indonesia, Thailand in 1997, and Ukraine) all ended in major financial crises and/or recessions following their runs. Even though all have seen their economies and financial sectors recover since, none have regained their peak credit/GDP ratio levels, including those that had set their peaks nearly 20 years ago. South Africa is a complex case, with massive economic inequality and the majority of its population having been excluded from active economic life during apartheid. It’s possible that at least some of the growth has been driven by post-apartheid financial inclusion. That said, there’s reason to think that its credit sector is too large, with a serious overindebtedness problem. On the positive side, two cases appear as success stories: China and the Philippines, which both saw relatively high growth that accompanied strong economic growth, with credit growth leveling off, then continuing at a slower rate. Neither country seems to have suffered significant consequences during the leveling-off period – the mild recession in the Philippines during the Asian financial crisis of 1998 stands in sharp contrast to the far more severe cases of its neighbors. Two other cases – Cambodia’s immediate neighbors Thailand (since 2001) and Vietnam – have seen even faster runs than China and the Philippines, and both levelled off without significant economic consequences. Vietnam’s banking sector has suffered significant NPLs, but the broader economy was only mildly affected. It’s perhaps not a coincidence that both border Cambodia, which seems to be influenced by its neighbors’ experience. So what do Thailand and Vietnam say about Cambodia? I’m no expert on southeast Asian economies, but it’s worth noting that both its neighbors, whose state banks play a major role in lending, differ greatly from Cambodia, where lending comes mainly from a highly competitive private sector of mid-sized banks and MFIs. The dynamics of these financial sectors are very different, as are the risks. Which of the above paths is Cambodia likely to follow? The success stories of China, Philippines, Vietnam, and Thailand (since 2001)? The crisis cases of Bolivia, Bosnia, Indonesia, Thailand in 1997, and Ukraine? Or the in-between story of South Africa and its struggles with overindebtedness? Such comparisons aren’t easy, but the fact that the available historical examples feature more failures than successes, should be reason alone to re-evaluate what is an undeniably high risk path. Back in 2005, when Cambodia’s financial sector took off, it was deeply under-developed and the rapid growth was playing catch up. For over a decade, that worked perfectly well, but what seems clear at this point is that not only has Cambodia caught up with its peer, but for the past several years it has been surpassing them along nearly every possible indicator of penetration and growth. For institutions that grew up in this environment, the expectations of that growth are now deeply ingrained. Yet it is a mathematical certainty that at some point Cambodia’s financial sector will have to slow down. It’s simply not possible for credit to grow five times faster than GDP, without at some point hitting a wall. And hitting the wall will be a lot more painful than hitting the brakes… __________ [1] MIX Market and CMA; includes all ACLEDA loans (large and small), as per MIX Market reporting [2] Developing countries (Human Development Index < .75 in 2014), increase in credit/GDP ratio > 35 during any period of 10 years or less in 1980-2013.

Country

Armenia

2002-14

6%

45%

ongoing

Bolivia

1986-98

13%

64%

crisis

Bosnia

2001-08

26%

67%

crisis

Brazil

1990-93

42%

128%

hyperinflation symptom

Cambodia

2004-14

9%

54%

ongoing

China

1983-93

58%

98%

declined to 87% in 1994, then increase continues at a more modest pace

Indonesia

1987-97

25%

61%

crisis

Mongolia

2001-13

9%

62%

mild taper in 2014 (to 61%)

Nepal

2002-09

23%

59%

rebound from decline during 2000-02; value in 2000: 31%

Philippines

1986-97

15%

56%

modest recession during “Asian crisis” in 1998

Serbia

2002-10

17%

53%

rebound following drop during the Kosovo war. Level in 2000 was at 49%.

South Africa

1990-2001; 2002-07

81%

167%

two growth periods, with dip in 2001 (from 142 to 115) and in 2008; currently high concerns of over-indebtedness

Thailand

1981-97; 2001-13

41%

165%

first period ended in crisis (1998); second period began in 2001 and peaked at 154% (due to political crisis)

Ukraine

1996-2009

1%

91%

transition to market economy; major recession in 2009

Vietnam

1995-2010

18%

115%

decline since 2010 due to high NPLs

Zimbabwe

1999-2002

22%

104%

hyperinflation symptom

Leave A Comment